Read More

Recognized for AI Excellence at 2026 Globee® Awards - Read More

Unlock the Potential with a Step-By-Step Guide to Financial Software Development

Pratik Mistry

Updated: Jun 8, 2026

ON THIS PAGE

- Financial Software Development: What is It?

- Types of Financial Software

- Must-Have Features for Financial Software

- Compliance Requirements for Financial Software

- Impact of AI on Financial Software Development

- The Financial Software Development Process

- Technologies Used to Develop Financial Software

- The Financial Software Development Team

- The Cost of Financial Software Development

- Choosing the Right Financial Software Development Company

- Getting Started with Financial Software Development

ON THIS PAGE

- Financial Software Development: What is It?

- Types of Financial Software

- Must-Have Features for Financial Software

- Compliance Requirements for Financial Software

- Impact of AI on Financial Software Development

- The Financial Software Development Process

- Technologies Used to Develop Financial Software

- The Financial Software Development Team

- The Cost of Financial Software Development

- Choosing the Right Financial Software Development Company

- Getting Started with Financial Software Development

Financial Software is the New Trust Engine: Financial software in 2026 no longer “supports” finance, it is finance. It decides how money moves, how risk is assessed, and how trust is earned in real time, powering every transaction, loan, and investment at millisecond speed. But here’s the catch: most systems aren’t built for this level of pressure. Compliance tightens, fraud adapts, and scale exposes cracks that only show up when it is already expensive to fix them. This guide breaks down what financial software development really looks like today. We cover the key types, the compliance needs, the impact of AI, and what it truly costs to develop financial software in 2026.

Financial software development is no longer just about digitizing transactions. Data across fintech reports and studies suggests that in 2026, it is the infrastructure that determines whether a fintech business can operate at speed, satisfy regulators, prevent fraud, and build the kind of user trust that traditional banking took decades to earn.

The stakes are concrete. According to Fortune Business Insights, the global fintech market reached $460.76 billion in 2026, up from $394.88 billion in 2025. That growth doesn't happen by accident. It's built line by line in software that processes payments in milliseconds, applies machine learning to flag suspicious transactions before they are completed, and meets compliance standards that get stricter every year.

This guide covers everything you need to understand about financial software development. The insights below are based on our 26+ years of experience and having delivered 350+ custom solutions to fintech businesses.

What Is Financial Software Development?

Financial software development is the process of designing, building, testing, deploying, and maintaining software applications that handle financial operations, including payments, lending, investment management, risk assessment, compliance monitoring, and banking services.

What separates financial software development from standard software development is the constraint layer. Every design decision operates within a framework of regulatory requirements, security standards, and audit obligations that don't exist in most other software categories. After all, when it comes to finance software development, a missed compliance requirement isn't a bug to patch later, it's a regulatory breach, a potential fine, and in some jurisdictions, a license revocation.

The Financial Software Landscape: By the Numbers

Here’s where the financial software market stands as of Q2 2026:

- According to Market Reports World, the financial services software market is valued at $20,369.42 Million in 2026 and expected to rise to $39,585.87 Million by 2035

- There is a 78% cloud adoption in financial services software ecosystems

- 64% of enterprise financial systems use API-based integration

- Embedded finance market is projected to exceed $320 billion globally by 2030

- A Gitnux report revealed that 8 in 10 banks have implemented AI-driven software by 2025

- Finance firms face the second-highest breach costs across all industries, averaging $5.56 million per incident.

Taken together, these numbers point to a clear direction: financial software is becoming more connected, more intelligent, and more regulated at the same time. As systems scale and integrate deeper across ecosystems, security, compliance, and architecture decisions are increasingly being pushed to the earliest stages of development.

From our experience of driving digital transformation for several banking and financial software systems across payments, lending, and digital banking, we’ve consistently seen a common pattern: Compliance is often treated as a later-stage checkpoint rather than a design input.

In practice, this creates friction during audits and often leads to rework that could have been avoided. That’s why, we make sure that in regulated environments, compliance isn’t “added on” before release but is a part of how the system is structured from the start.

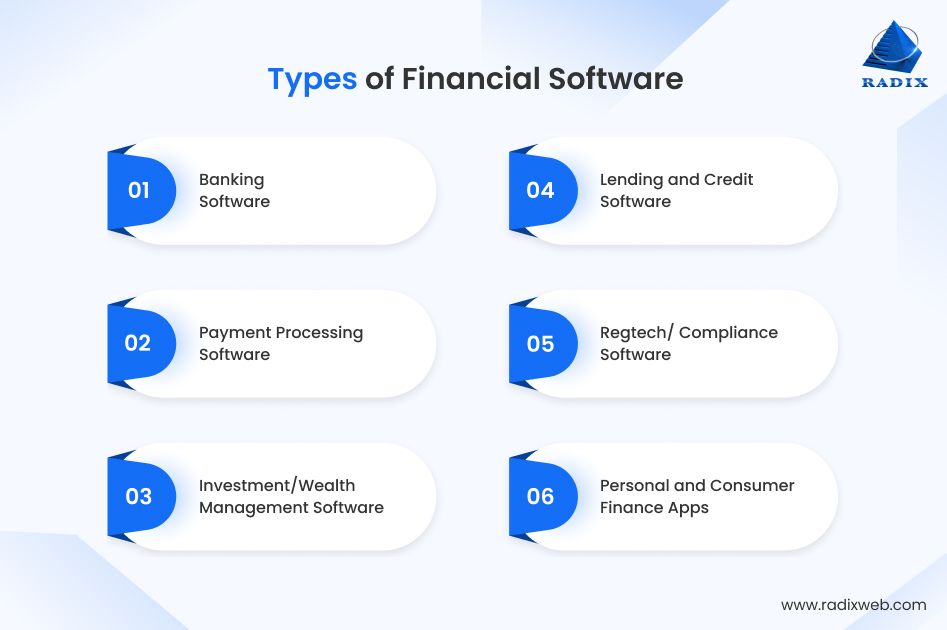

What Are the Types of Financial Software?

The financial technology (or Fintech) landscape is wide and expansive. Not all financial software is the same. The type of software your fintech business needs depends entirely on what financial problem you're solving, which regulations apply, and what user experience you're delivering. Here are the most common types of financial software solutions:

1. Banking and Core Banking Software

Core banking systems are the operational backbone of banks and neobanks. They handle account management, transaction processing, loan servicing, and customer records in real time. Legacy core banking systems, many built in the 1970s and 1980s, are actively being replaced by cloud-native, modular architectures. Neobanks and challenger banks built on modern core banking software and platforms can deploy new product features in days rather than the months a traditional bank requires.

The development challenge here is uptime and data integrity. Core banking systems typically require 99.99% availability and zero-error transaction processing, which demands architecture decisions that go far beyond standard application development.

2. Payment Processing Software

Payment software handles the technical plumbing of moving money: payment gateways, payment orchestration platforms, point-of-sale integrations, peer-to-peer transfers, and cross-border payment systems. This category is heavily regulated under PCI DSS (the Payment Card Industry Data Security Standard) and, for European markets, PSD2.

The 2026 shift in this category is real-time payment rails. Instant payment expectations, set by systems like FedNow in the US and SEPA Instant in Europe, mean that payment software must process and settle transactions within seconds rather than the traditional one-to-three business days.

3. Investment and Wealth Management Platforms

Robo-advisors, portfolio management systems, trading platforms, and digital wealth management tools fall into this category. These systems handle market data feeds, algorithmic trading logic, portfolio rebalancing, and client reporting.

Robo-advisors were handling over $1.0 trillion in assets globally by 2025. Development in this space requires expertise in financial data modeling, real-time market data integration, and audit-trail requirements for every portfolio action.

4. Lending and Credit Software

Loan origination systems, credit scoring engines, underwriting platforms, and BNPL (Buy Now Pay Later) infrastructure are built in this category. The critical development challenge however is the credit decision logic: the software must make fair, explainable lending decisions that satisfy consumer protection regulations including ECOA in the US and the Consumer Credit Directive in Europe.

AI-driven credit scoring is reshaping this space. Machine learning models that analyze alternative data sources, such as transaction history and cash flow patterns, produce more accurate risk assessments than traditional credit bureau scores for underbanked populations. But building these models requires careful attention to bias testing and regulatory explainability requirements.

5. RegTech and Compliance Software

Regulatory technology is now automating compliance workflows that would otherwise consume enormous manual effort. This includes AML (anti-money laundering) monitoring, KYC (know your customer) identity verification, sanctions screening, transaction reporting, and audit trail management.

In 2026, with regulatory complexity increasing across jurisdictions, RegTech is one of the fastest-growing sub-segments of financial software. The DORA regulation (Digital Operational Resilience Act) in Europe, which came into full effect in January 2025, added mandatory ICT risk management, incident reporting, and third-party vendor resilience requirements for financial entities. Every financial software system operating in European markets must be built with DORA compliance in mind.

6. Personal Finance and Consumer Financial Apps

Budgeting tools, expense trackers, savings apps, and financial wellness platforms serve individual consumers rather than enterprises. The development focus here is user experience, data aggregation through open banking APIs, and behavioral design that drives healthy financial habits.

Open banking has fundamentally changed this category. By accessing transaction data through regulated API connections rather than screen scraping, personal finance apps can deliver accurate, real-time financial views without the security risks of stored credentials.

Key Features Every Financial Software System Needs

While every category of financial software comes with its own unique feature set that often becomes its core USP, there’s a shared baseline that cannot be ignored. These are not differentiators but expectations. Customers assume they will be there, and regulators require them to be in place before the system can operate safely.

Here are some of those foundational features that every software being built for the finance field must have, regardless of its use case.

Secure Authentication and Identity Management

Multi-factor authentication, biometric verification, and adaptive authentication that escalates security requirements based on transaction risk are now baseline requirements in 2026. PSD2's Strong Customer Authentication (SCA) mandate requires MFA for any payment above low-risk thresholds across European markets.

Beyond login, financial software needs continuous session authentication, detecting behavioral anomalies that might indicate account takeover even after initial login succeeds.

Real-Time Fraud Detection

Static rule-based fraud detection is a 2015 approach. In 2026, fraud detection in financial software is machine learning at the transaction layer: models that evaluate hundreds of signals per transaction in milliseconds, flagging suspicious patterns before the transaction settles. Today, AI in fraud detection is moving from basic automation to adaptive, real-time intelligence that improves onboarding accuracy and strengthens risk management.

Compliance and Audit Trails

Every significant action in a financial system, every transaction, every configuration change, every data access event, must be logged with timestamp, user identity, and system state in a tamper-evident audit trail. Regulators don't just audit outcomes, they audit the process. A system that can't produce a clean audit trail for any time window, on demand, will fail its first compliance review.

Data Encryption and Security Architecture

Encryption at rest and in transit is not a feature. It's a foundation. Financial software in 2026 applies field-level encryption for sensitive data like account numbers and personal identifiers, tokenization for payment card data, and hardware security modules (HSMs) for cryptographic key management in high-value systems.

API-First Architecture for Integration

Financial software doesn't exist in isolation. It connects to payment networks, credit bureaus, identity verification providers, regulatory reporting systems, and increasingly to embedded finance partners. An API-first architecture makes these integrations maintainable, auditable, and extensible without requiring core system changes for each new connection.

Scalable Transaction Processing

A payment system that processes 1,000 transactions per day and one that processes 1,000,000 transactions per day are architecturally different products. Financial software must be designed for the transaction volume ceiling of the business at scale, not the volume at launch. Designing for scale after the fact is significantly more expensive than building it in.

The above-mentioned features are a must-have for financial software, but if you are looking at true success and market dominance, you need to go beyond the basics. Below are a few examples of financial software solutions that we have developed in the past couple of years, where these baseline features are present, along with additional capabilities tailored to specific business needs.

| Project | Core Financial Context | Unique / Differentiating Features |

|---|---|---|

| Digital Mortgage Platform for FinTech Company | End-to-end mortgage lending automation | Blockchain-based record integrity, AI-driven risk assessment, OCR-based document verification, real-time loan tracking |

| Loan Management System for Construction Lending | Construction project-based lending and fund tracking | Real-time project visibility, fund disbursement tracking, risk monitoring across project stages, field inspection integration |

| Custom Loan Management System (Lending Platform) | Digital lending and loan lifecycle management | Automated loan approval workflows, centralized data intelligence, compliance risk mitigation module, scalable cloud-based architecture |

These examples show how even with the same foundational requirements each solution builds its differentiation through business-specific workflows and features.

The 2026 Compliance Architecture: What Financial Software Must Satisfy

In the past couple of years, regulatory compliance has emerged as one of the key challenges of developing software for the finance industry. Understanding the current standards is not optional anymore and fintech companies need to ensure adherence to avoid regulatory action.

What Compliance Standards Apply to Financial Software?

The applicable standards depend on geography, product type, and user category, but the following are the baseline requirements for most financial software in 2026:

- PCI DSS 4.0 (effective March 2025) introduced significant changes from version 3.2.1, including more flexible implementation options for meeting requirements, stronger authentication standards, and new requirements specifically targeting eCommerce and API-based payment environments. Any software that touches payment card data must be PCI DSS 4.0 compliant.

- PSD2 and Open Banking mandates in Europe require financial software to expose customer data to authorized third parties through regulated APIs. Building PSD2-compliant APIs requires specific authentication flows, consent management infrastructure, and data portability capabilities.

- DORA (Digital Operational Resilience Act) applies to all financial entities and their ICT service providers operating in the EU. It requires documented ICT risk management frameworks, mandatory incident reporting within defined timeframes, and resilience testing including penetration testing of critical systems. Software built for EU financial markets must be designed with DORA's operational resilience requirements as first-class architectural requirements, not compliance add-ons.

- GDPR governs personal data handling for any system processing EU resident data. For financial software, this includes the right to erasure (complex in systems with immutable audit trails), data minimization requirements, and explicit consent management.

- AML/KYC regulations require financial software to verify customer identities, screen against sanctions lists, and monitor transactions for money laundering patterns. The software implementation of these requirements must produce documentation sufficient for regulatory examination.

Together, these standards increasingly shape not just what financial software does, but how it is designed, integrated, and scaled from the very beginning.

How AI Is Changing Financial Software Development

The financial technology market is seeing several new and emerging trends and AI remains the most dominant among those.

The AI in financial services market is valued at over $390 billion in 2025 and is expected to be worth $3497 billion by 2033. This 30%+ CAGR is evident in how rapidly financial institutions are moving from experimentation to full-scale deployment.

It makes one thing clear: AI is no longer a “nice-to-have” layer added on top of financial software. AI is now the core architecture of finance and it is shaping how data is processed, how decisions are made, and how systems operate under real-world financial and regulatory pressure, which brings us to a very important question:

How Does AI Improve Financial Software?

AI adds value, in multiple ways, to any software solution it is embedded or integrated it. Specifically for financial software, here’s where the AI’s maximum value lies:

- Fraud detection is the most mature AI application. Machine learning models running at transaction time evaluate behavioral patterns, device fingerprints, network signals, and transaction history simultaneously to score fraud risk in under 100 milliseconds. These models catch fraud patterns that rule-based systems miss, while producing fewer false positives that frustrate legitimate customers.

- Credit scoring and underwriting using alternative data sources, transaction behavior, cash flow patterns, and bill payment history enable more accurate risk assessment for thin-file applicants who don't have traditional credit history. The regulatory challenge is explainability: AI credit decisions must be explainable to applicants and defensible to regulators under equal credit opportunity laws.

- KYC and onboarding automation now uses AI-driven document verification and biometric matching to verify identity in seconds rather than days. AI in finance and banking is increasingly focused on AML, KYC, and KYB tools moving from basic automation to adaptive, real-time intelligence.

- Personalized financial advice at scale, previously available only through human advisors to high-net-worth clients, is being delivered to retail users through AI-powered guidance in personal finance and banking apps.

But that’s not all. On the development side too, the implications of AI in financial software are significant. AI is being used to speed up financial software development. Also, this AI-generated code requires heightened code review because the cost of a logic error in a financial system is not just a bug report but potential financial loss or compliance breach.

To mitigate such risks, at Radixweb, all our AI-assisted code goes through additional review stages beyond standard code review. This helps ensure focus on validating correctness, traceability, and edge-case behavior before deployment.

The Financial Software Development Process: Stage by Stage

Developing financial software solutions for banks, lending institutions or other market players follows a structured process where security, compliance, scalability, and reliability are built into every stage from the beginning.

Stage 1: Discovery and Requirements Engineering

A proper discovery phase specifically maps the regulatory environment your software must operate in before any architecture decisions are made. Which jurisdictions will your users be in? Which payment networks will you connect to? Which data categories will you process? The answers determine the compliance framework, which determines the architecture, which determines the build.

This stage should produce a detailed requirements document, a compliance obligation map, a preliminary data flow diagram, and an initial security threat model. Skipping any of these produces technical debt measured in months of rework, not days.

Stage 2: Architecture and System Design

Financial software architecture is not standard application architecture with security bolted on. It's security and compliance architecture with application features built inside.

Key decisions at this stage include:

- Monolith vs. microservices (microservices offer better isolation of compliance domains but higher operational complexity),

- Cloud provider selection (each major provider has different compliance certifications, relevant to regulated workloads),

- Data residency architecture (many financial regulations require data to remain within specific geographic boundaries), and

- Encryption architecture (which data requires field-level encryption vs. transport-level encryption).

The API design decisions made here determine the cost of every integration the system needs to support over its lifetime. An API-first design with well-documented, versioned interfaces is standard practice in 2026 fintech development. Open banking, embedded finance, and Banking-as-a-Service all run on API architectures.

Stage 3: Development with Continuous Security Integration

Financial software development today uses DevSecOps as the default delivery model. Security scanning runs on every code commit. Static analysis identifies vulnerabilities in dependencies before they reach staging. Secret scanning prevents credentials from being committed to version control.

The development sequence for most financial software follows compliance priority: authentication and authorization infrastructure first, followed by core transaction logic, then reporting and audit trail systems, then user-facing features. This sequence ensures that the security and compliance foundation is in place before features are built on top of it.

Stage 4: Testing for Security, Compliance, and Performance

Testing financial software requires more than functional QA. It requires a dedicated security testing phase including penetration testing, vulnerability scanning, and threat modeling validation. For payment software, PCI DSS requires annual penetration testing by a qualified security assessor. DORA requires documented resilience testing for EU financial entities.

Performance testing is critical at realistic transaction volumes. A payment system that processes 500 transactions per second in staging but fails at 5,000 in production is not a testing problem. It's an architecture problem that surfaces late and expensively.

Compliance testing validates that the software's actual behavior matches its regulatory commitments: that consent flows produce correct audit records, that fraud detection thresholds produce legally compliant decision documentation, that data deletion requests are handled correctly across all data stores.

Stage 5: Deployment and Infrastructure

Successful financial software deployments are never a push to production but always a controlled promotion process with security review gates at each environment boundary. Blue-green deployment or canary releases reduce the risk of production incidents by limiting blast radius when new versions are introduced.

Infrastructure choices for financial software in 2026 are predominantly cloud-native, with hybrid configurations for organizations that must maintain on-premises components for regulatory reasons. Cloud providers including AWS, Azure, and GCP offer compliance-accelerating managed services for encryption, key management, audit logging, and identity management that reduce the build overhead of compliance infrastructure.

Stage 6: Monitoring, Maintenance, and Ongoing Compliance

Financial software doesn't reach a stable compliance state. Regulations change. Threat landscapes evolve. Vendor dependencies release security updates. A financial software system without a structured maintenance and monitoring program drifts out of compliance incrementally.

Monitoring for financial software includes:

- Application performance monitoring

- Security event monitoring

- Fraud signal monitoring

- Regulatory reporting monitoring

Incident response plans must be documented and tested before a system enters production, because DORA requires financial entities to notify regulators of significant ICT incidents within defined timeframes, which requires incident classification workflows to exist before incidents occur.

What Tech Stack Is Used for Financial Applications?

The right technology stack for financial software depends on the system type, transaction volume, and regulatory environment. The following patterns are prevalent in 2026:

| Category | Important For | Technologies Used |

|---|---|---|

| Backend Systems | Core application logic handling transactions, workflows, and business rules under high reliability and consistency requirements | Java, Python, Node.js, Go |

| Cloud Infrastructure | Hosting and scaling environment designed to meet compliance, latency, and data residency requirements | AWS, Microsoft Azure, Google Cloud, hybrid cloud setups |

| Databases & Data Layer | Storage systems optimized for transactional integrity, real-time processing, and high-volume financial data handling | PostgreSQL, Cassandra, TimescaleDB, Redis |

| Security Infrastructure | Systems responsible for encryption, access control, and secure credential management across the application | HashiCorp Vault, Hardware Security Modules (HSMs), IAM systems, TLS/SSL encryption frameworks |

| APIs & Integration Standards | Connectivity layer enabling interoperability between banks, fintech platforms, and external financial systems | REST APIs, OAuth 2.0, OpenID Connect, FDX APIs, Berlin Group PSD2 APIs |

Remember: The ideal financial software development stack is less about individual technologies and more about how they are combined to meet financial-grade reliability, security, and compliance demands in production environments.

What Is the Cost of Financial Software Development?

The cost of financial software development varies significantly based on system complexity, compliance requirements, team location, and whether you're building a new product or modernizing an existing system.

Realistic 2026 ranges by system type:

| System Type | Complexity | Estimated Range |

|---|---|---|

| Personal finance / budgeting app | Low-medium | $80K - $200K |

| Payment gateway integration | Medium | $150K - $400K |

| Digital banking platform (neobank MVP) | High | $400K - $1.2M |

| Core banking system modernization | Very high | $1M - $5M+ |

| Full trading / investment platform | High-very high | $500K - $2M+ |

| RegTech compliance automation | Medium-high | $200K - $800K |

These ranges assume professional development teams, proper security architecture, and compliance infrastructure built from the start. They do not include ongoing operational costs, regulatory certification fees, or post-launch maintenance.

The single largest driver of financial software development cost is compliance. But you shouldn’t skip on that to reduce the cost because adding compliance later on costs way more than the initial build. A payment system built without proper PCI DSS architecture costs far less in the initial build and far more in the remediation, re-audit, and potential fine exposure when the compliance gap is discovered. So, building compliance from the start is always the lower total cost option.

Team Composition for Financial Software Development

A financial software project requires specialist developers with fintech expertise that a standard software team doesn't typically include. You need a team that includes:

- A financial software architect who understands both the technical architecture and the regulatory environment. This role is different from a standard solutions architect because compliance requirements directly influence architecture decisions.

- Security engineers with financial services experience, specifically knowledge of PCI DSS implementation, threat modeling for financial systems, and penetration testing of payment flows.

- Compliance engineers or consultants who translate regulatory requirements into technical specifications. Many development teams are strong on technical skills but lack the regulatory domain knowledge to correctly interpret what a specific compliance requirement means for their architecture.

- QA engineers with security testing experience, including penetration testing and compliance validation in addition to standard functional testing.

In practice, you need a financial software development team with both engineering depth and regulatory understanding, since many technical decisions have direct compliance implications.

Choosing the Right Financial Software Development Partner

Financial software can be built through three common approaches: an in-house team, independent freelancers/contractors, or a specialized development partner for building custom solutions. The right choice depends on the complexity of the product, regulatory exposure, budget, and delivery timelines.

| Option | Best Suited For |

|---|---|

| In-House Team | Long-term product ownership, highly proprietary platforms, organizations with existing engineering maturity |

| Freelancers / Contractors | Small MVPs, limited-scope integrations, early-stage validation projects |

| Financial Software Development Partner | Compliance-heavy systems, faster go-to-market needs, products requiring specialized fintech expertise |

For most financial software projects, choosing a fullstcak development partner specializing in finance projects tends to make the most operational sense. Financial systems rarely require just developers. They also need security engineering, compliance understanding, cloud infrastructure expertise, testing maturity, and experience with regulated workflows. Building all of this internally takes significant time and coordination, while freelancers are usually optimized for narrower execution scopes rather than end-to-end ownership in regulated environments.

That said, the market has no shortage of development companies with fintech expertise. The challenge is identifying which teams can actually handle the technical and compliance complexity financial systems demand. Here are the best practices for finding companies that fit your needs:

- Evaluate their experience with regulated financial systems

- Verify familiarity with standards like PCI DSS, GDPR, PSD2, AML/KYC, or DORA

- Review case studies from similar financial product categories

- Assess their security engineering and testing practices

- Understand their cloud, scalability, and infrastructure capabilities

- Clarify IP ownership, documentation access, and long-term support models

- Check whether they can support the full lifecycle from architecture to maintenance

Ultimately, the right partner is not just the one that can build features fastest, but the one that can help the software remain secure, scalable, and compliant as the business grows.

Build a Compliance-First Financial System Designed for Growth

The financial software companies scaling successfully in 2026 are not just building faster, they are building with long-term resilience in mind from day one. That means developing tailored financial software solutions that can adapt to changing regulations, support new financial models, integrate with evolving ecosystems, and handle increasing transaction complexity without constant architectural rework.At Radixweb, financial software projects are approached with that long-term view from the beginning. Our teams work across architecture planning, compliance-aware engineering, cloud-native infrastructure, and secure product development to help fintech businesses build systems that are production-ready from both a technical and regulatory standpoint.With experience across lending, payments, digital banking, and other regulated domains, the focus remains on building software that can evolve with the business instead of limiting it later. Schedule a consultation with our financial software experts to evaluate your product strategy, compliance requirements, and technology roadmap before development begins.

Frequently Asked Questions

How long does it take to build financial software?

What features should financial software have?

What programming languages are used for financial software?

How do you choose a financial software development company?

What is the difference between RegTech and standard financial software?

Explore More Topics

Ready to brush up on something new? We've got more to read right this way.

Get top Insights and news from our technology experts.