Read More

Recognized for AI Excellence at 2026 Globee® Awards - Read More

Fintech Software Development in 2026: The Complete Business Guide

Pratik Mistry

Updated: Mar 27, 2026

ON THIS PAGE

- What is Fintech Software Development?

- Why Invest in Fintech Software in 2026?

- What are the Types of Fintech Software?

- What are the Key Fintech Development Trends in 2026?

- What are the Must-Have Features for Fintech Products?

- What are the Most Important Fintech Regulations?

- What is the Cost of Fintech Development in 2026?

- Building Fintech In-House vs. Hiring a Fintech Software Development Company

- How to Select the Right Fintech Software Development Company

- What are the Top Fintech Development Challenges?

- What is the Fintech Software Development Process?

- What’s Next in Fintech Software Development?

- Why Radixweb is Your Ideal Fintech Software Development Partner?

ON THIS PAGE

- What is Fintech Software Development?

- Why Invest in Fintech Software in 2026?

- What are the Types of Fintech Software?

- What are the Key Fintech Development Trends in 2026?

- What are the Must-Have Features for Fintech Products?

- What are the Most Important Fintech Regulations?

- What is the Cost of Fintech Development in 2026?

- Building Fintech In-House vs. Hiring a Fintech Software Development Company

- How to Select the Right Fintech Software Development Company

- What are the Top Fintech Development Challenges?

- What is the Fintech Software Development Process?

- What’s Next in Fintech Software Development?

- Why Radixweb is Your Ideal Fintech Software Development Partner?

Before you scroll past this: Written for business decision-makers, product owners, founders, and C-suite executives, this guide explains fintech software development from a business perspective. You will learn what it costs, what compliance actually demands from your architecture, which solution types make the most commercial sense in 2026, and how to choose a development partner who has genuinely navigated regulatory audits, not just listed compliance in their service portfolio. These insights come directly from our 26+ years of experience building enterprise fintech products.

What Is Fintech Software Development?

Fintech software development is the process of designing, building, and deploying digital products that deliver financial services through software. It includes a wide range of digital financial solutions including mobile banking apps, payment gateways, AI-powered lending platforms, digital wallets, insurance platforms, and wealth management tools.

Important: During initial project discussions, a lot of clients feel that fintech software development is the same as any other software development projects. That’s not true. Fintech software development is fundamentally different because it operates at the intersection of finance, regulation, and technology. So, fintech products must simultaneously be secure enough to protect user funds and data, compliant enough to satisfy regulators across one or multiple jurisdictions, and fast enough to meet the expectations of users who now treat sub-second transaction speeds as a baseline.

In recent years, particularly 2025 and 2026, fintech software development has become more strategically important than ever. Banks, retailers, healthcare platforms, and insurance companies are all investing in custom financial software because off-the-shelf tools are noticeably failing to keep up with the compliance complexity or the customer experience expectations that define this market.

So, whether you are building a fintech product from scratch, expanding your existing financial platform, or looking for a team that has delivered regulated financial software across banking, payments, and lending at scale, this guide brings together everything you need to understand.

The Business Case for Fintech Investment in 2026

The recent growth in Fintech has been reflecting a very genuine, durable shift in how people and businesses manage money.

- The global fintech market was valued at approximately USD 394.88 billion in 2025 and is projected to reach USD 1760.18 billion by 2034, growing at a CAGR of 18.20%. (Fortune Business Insights)

- Global fintech funding reached USD 44.7 billion across 2,216 deals in H1 2025 alone (KPMG).

- The embedded finance market is projected to exceed USD 155 billion by the end of 2026. (Mordor Intelligence)

- Digital wallets are on track to serve more than two-thirds of the global population by 2029. (Juniper Research)

- Digital payment transactions are projected to reach USD 26.89 trillion in transaction value in 2026. (Statista)

These numbers make it very clear: The window to build competitive fintech products is narrowing, definitely not widening. The companies that invest in custom fintech software development today are building moats that will be very difficult to close two to three years from now.

Types of Fintech Software Solutions: What Businesses Are Building

Fintech software development covers a wide range of product categories. Knowing which type of fintech software solution best fits your business model and target market is important. It's the first strategic decision you need to make before any development begins, as it directly impacts your product scope, compliance requirements, and long-term cost structure.

Quick Overview

| Type | Primary Use Case | Revenue Model | Complexity |

|---|---|---|---|

| Digital Banking | Full-service banking apps | Fees, lending | High |

| Payments | Transactions, wallets | Transaction fees | Medium |

| Lending | Credit & BNPL | Interest, fees | High |

| InsurTech | Claims & underwriting | Premiums | Medium |

| WealthTech | Investment platforms | AUM, commissions | Medium |

| RegTech | Compliance automation | SaaS | Medium |

| Embedded Finance | Finance inside apps | Revenue share | High |

Digital Banking Software

Digital banking platforms allow users to open accounts, transfer funds, apply for loans, and manage their financial lives entirely through a mobile or web interface. Neobanks like Revolut, N26, and Chime built their entire businesses on this model.

- Why demand is growing in 2026: A significant share of the global population remains underserved by traditional banking infrastructure. Digital-only banking fills that gap at a fraction of the cost of physical branch networks.

- What to know before you build: Digital banking software is the most technically demanding and commercially complex category to build, which is why teams evaluating this path typically begin by reviewing what modern banking software development actually involves before committing to a scope. It carries the broadest feature scope and the deepest regulatory compliance requirements of any product type in this guide. Budget and timeline expectations must reflect that reality from day one.

- Key business metrics to track: Customer acquisition cost, monthly active users, average revenue per user, loan book performance, and compliance incident rate.

Payment Processing Software

Payment platforms handle the movement of money between parties, whether peer to peer, business to consumer, or business to business. This category includes digital wallets, payment gateways, cross-border remittance platforms, and buy now pay later infrastructure.

- What changed in 2026: Real-time payment processing is no longer a differentiator. It is the default expectation. The EU Instant Payments Regulation (adopted 2024) mandates instant euro credit transfers across the eurozone. Similar regulatory shifts are accelerating in Asia, the UK, and North America.

- Business model: Transaction fees, payment margin, white-label licensing.

Lending and Credit Platforms

Digital lending software covers personal loan apps, small business lending platforms, buy now pay later solutions, and AI-powered credit decisioning tools. The commercial opportunity here is significant.

- The competitive reality in 2026: AI-powered credit decisioning platforms are approving loan applications in minutes. Businesses still running manual underwriting are losing customers to platforms that deliver instant decisions, and many are turning to AI-powered capabilities built into their financial software to close that gap quickly. If you are in financial services and have not automated your underwriting process, you are already behind.

- Business model: Interest income, origination fees, data licensing.

InsurTech Software

Insurance technology platforms are transforming how insurers price risk, process claims, and engage with customers. Telematics platforms that use real-time data from connected devices to price motor insurance dynamically, AI-powered claims processing systems, and digital broker platforms are all growing categories within InsurTech.

- Why investment is growing in 2026: The business case is clear. AI-driven underwriting reduces loss ratios. Digital claims processing cuts settlement times from weeks to hours. Customer experience improvements drive measurable retention gains.

- Business model: Policy premiums, claims management fees, platform licensing.

WealthTech and Investment Platforms

Wealth management software includes robo-advisors, portfolio management platforms, personal finance management tools, and retail investment apps. These platforms are democratizing access to investment services by removing minimum investment thresholds and the need for human financial advisors.

- The battleground in 2026: AI-powered personalization. Platforms delivering genuinely individualized financial recommendations at scale are capturing market share from incumbents that still rely on human advisors and one-size-fits-all products.

- Business model: AUM-based fees, subscription tiers, transaction commissions.

RegTech Software

Regulatory technology platforms automate compliance processes including Know Your Customer verification, Anti-Money Laundering screening, transaction monitoring, and regulatory reporting.

- The business case in one sentence: The cost of a compliance failure dwarfs the cost of the RegTech investment that would have prevented it.

- Why it is one of the fastest-growing fintech categories in 2026: Global regulatory complexity increased sharply with DORA, MiCA, and intensified GDPR enforcement. Manual compliance processes cannot keep pace. Automation is no longer optional.

Embedded Finance and Banking as a Service

Embedded finance is the integration of financial services directly into non-financial platforms. A retail platform offering consumer credit at checkout, a ride-sharing app providing instant driver payouts, a healthcare platform offering patient financing for procedures. These are all examples of embedded finance.

- Market size: The embedded finance market is projected to exceed USD 250 billion by 2030, growing at a CAGR of 21.5% between 2026 and 2030.

- Why it matters more than any other trend on this list: Embedded finance is the single most transformative structural shift in financial services of the past decade. For businesses outside traditional finance, it is a revenue diversification opportunity. For traditional financial institutions, it is a distribution challenge that demands API-first architecture and BaaS capability now, not later.

Cryptocurrency and Blockchain Platforms

Crypto and blockchain-based fintech products include digital asset exchanges, crypto wallets, DeFi platforms, and tokenized asset products.

- The critical 2026 compliance shift: MiCA (Markets in Crypto-Assets Regulation) created a mandatory licensing regime for crypto-asset businesses across the EU, with the transitional period running through mid-2026. Businesses still assessing their obligations can review the official MiCA regulatory framework published by the European Securities and Markets Authority. After that, unlicensed operation is not permitted.

- Business implication: Regulatory compliance is now the primary product design constraint for crypto and blockchain fintech, and businesses in this space increasingly work with specialists in crypto and blockchain platform engineering who understand how to architect for MiCA requirements from the ground up. It is not an afterthought. Build the compliance architecture first or do not build at all.

The Fintech Software Development Landscape in 2026: Key Trends Every Business Must Understand

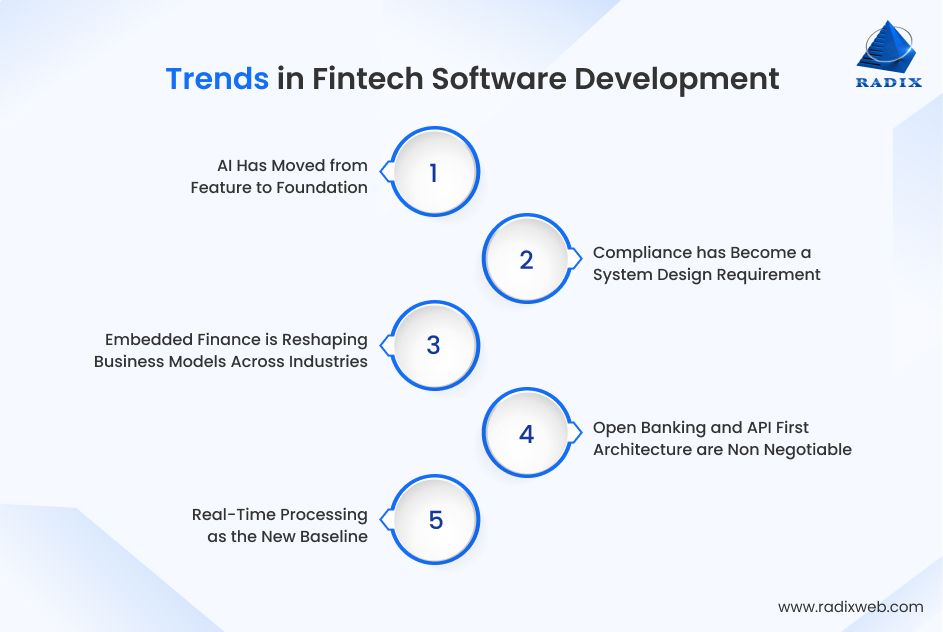

The rules of fintech changed in 2025 and they are not changing back in 2026 or beyond. AI is now the operational core, not a feature layer. Compliance is a system design constraint, not a legal checklist. Real-time processing is the baseline, not a differentiator. I am seeing a marked shift in how successful fintech products are built, delivered and scaled. Below, I discuss the most prominent macro trends of fintech software development that I see across the industry and how these should guide your roadmap and technology investments.

1. AI Has Moved from Feature to Foundation

A few months ago, AI used to be a feature you add to a fintech product, an add-on. In 2026, it’s the operational core. Modern financial products are built on AI capabilities like real-time fraud detection to automated underwriting. And it isn’t just a few use cases, AI is actually transforming banking and financial services as a whole.

Where AI is being deployed right now:

- Real-time fraud detection and transaction monitoring

- Credit risk modeling and automated underwriting

- Document processing and KYC verification automation

- Personalized customer engagement at scale

- Internal compliance workflows and regulatory reporting

Market size: The AI in fintech segment is projected to grow at a 14.5% CAGR between 2026 to 2033.

The most important AI development in fintech in 2026:

Agentic AI. These are AI systems that autonomously execute complex, multi-step financial workflows with minimal human intervention. Unlike earlier AI tools that assisted human decisions, agentic AI makes and acts on decisions independently.

Where agentic AI is already operating in production:

- Automated loan origination from application to approval

- Real-time regulatory reporting without human review

- Intelligent customer onboarding flows that adapt to user behavior

What this means for your business:

If your fintech product does not have a clear AI integration roadmap today, you are building to a standard that will be commercially obsolete within 18 to 24 months and integrating AI into existing financial platforms and workflows is now a standard part of product modernization rather than a future initiative. What (AI capability) was once a competitive advantage in fintech has become the entry requirement.

2. Compliance Has Become a System Design Requirement

Regulatory complexity in fintech reached a new threshold in 2025 and 2026. Three developments every business building financial software must understand:

DORA (Digital Operational Resilience Act) Came into force across the EU in early 2025. Imposes strict IT risk management requirements on financial institutions and their technology partners. If you work with EU financial institutions, DORA applies to you regardless of where your business is headquartered.

MiCA (Markets in Crypto-Assets Regulation) Created a mandatory licensing regime for crypto-asset businesses across the EU. The 18-month transitional period runs into mid-2026. No license after that date means no operation.

GDPR Enforcement Intensified significantly in 2025. Fines are increasing materially for organizations that cannot demonstrate data residency compliance and processing transparency. Financial companies are among the most frequently targeted.

The practical implication for your build:

Compliance cannot be bolted onto a fintech product after it is built. It must be designed into the architecture from day one, covering data storage decisions, audit trail infrastructure, API access controls, and reporting pipelines.

The cost of getting this wrong:

Financial institutions that treat compliance as a box-checking exercise rather than a system design constraint consistently spend two to three times more on remediation than compliance-by-design would have cost from the outset.

If your development partner is not talking about compliance architecture in the first conversation, find a different development partner.

3. Embedded Finance Is Reshaping Business Models Across Industries

Launching new fintech companies used to be the dominate trend in fintech. The most significant fintech trend in 2026, however, is non-financial businesses integrating financial services directly into their existing products.

What this looks like in practice:

- Retailers adding buy now pay later at checkout

- Employers offering earned wage access to staff before payday

- B2B software platforms offering revenue-based financing to their SME customers

- Healthcare providers embedding patient payment plans inside appointment booking flows

- Logistics companies offering invoice financing to suppliers inside their procurement portal

Why each of these is a serious business opportunity, not a technology experiment:

Each example above has three things that most fintech startups spend years trying to acquire: a clear business case, a captive user base, and a defined distribution advantage. The financial product rides an existing relationship. The trust is already there.

What this means if you operate a platform:

If your business has meaningful transaction volume, recurring user engagement, or proprietary financial data, you already have the raw ingredients for an embedded finance product — one that typically requires the kind of custom financial software built around your specific business model and compliance posture.

Instead of wondering whether embedded finance is relevant to your business, your question should be how quickly you can build the API-first architecture required to take advantage of it before a competitor does it first.

The businesses capturing that revenue are not all traditional financial institutions. Most of them started as retailers, SaaS platforms, and marketplaces.

4. Open Banking and API-First Architecture Are Non-Negotiable

Open banking mandates have matured across every major market. This is no longer an emerging trend. It is an operating requirement.

What is in force right now:

- PSD2 (Europe): Mandates that banks expose account data and payment initiation to licensed third parties via open APIs

- Consumer Data Right (Australia): Gives consumers the right to share their financial data with accredited third parties

- Open Banking Framework (UK): Requires the nine largest UK banks to share customer data through standardized APIs

- Account Aggregator Framework (India): Enables consented financial data sharing across banks, insurers, and lenders

What winning fintech businesses did differently:

The companies dominating fintech in 2026 did not retrofit API connectivity after launch. They built their entire architecture API-first from day one, making integration with banking rails, payment networks, and third-party services frictionless from the moment their products went live.

What API-first architecture delivers for your business:

- Faster time to market for new financial features

- Lower integration costs when onboarding banking and payment partners

- Easier compliance with open banking mandates across multiple markets

- A foundation for embedded finance and BaaS products built on top of your core platform

The business risk of getting this wrong:

A fintech product built on a closed, proprietary architecture in 2026 is a product that will require expensive re-architecture within two to three years. The cost of building API-first from the start is a fraction of the cost of rebuilding later.

5. Real-Time Processing as the New Baseline

User expectations around transaction speed have reset permanently. There is no going back.

The new standard in 2026:

- A payment that takes more than a few seconds is not slow. It is broken.

- Fraud detection that does not operate in real time is not fraud detection. It is incident reporting after the fact.

- An API response time above one second is not a performance issue. It is a product failure.

What real-time processing requires from your architecture:

- High-throughput backend infrastructure designed for concurrent transaction volume, not average load

- Event-driven architecture that processes and responds to transactions as they happen

- Automated failover with no single points of failure

- Edge computing or regional cloud deployment to minimize latency across geographies

- Continuous performance monitoring with automated alerting before users notice degradation

Why this matters as a business decision, not just a technical one:

Real-time processing capability directly affects three commercial metrics that determine whether your fintech product survives:

User acquisition: Slow products do not get recommended. They get abandoned and reviewed negatively. User retention: A single failed or delayed transaction in a financial product destroys trust that took months to build. Regulatory standing: Several jurisdictions now include performance and availability standards in their financial software licensing requirements.

Real-time processing is not a feature on your product roadmap. It is a prerequisite for being in the market at all.

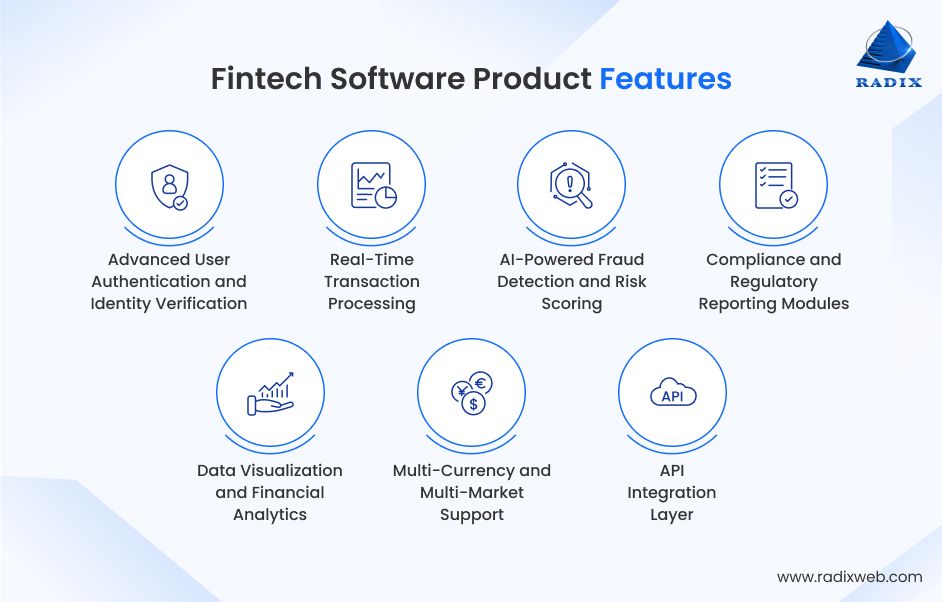

Must-Have Features for Fintech Software Products

If you think you can do the bare minimum now and add compliance, AI and governance related features later on, you need to rethink your fintech strategy. What you see before are features that are non-negotiable for any fintech product that expects to acquire users, satisfy regulators, and compete commercially.

If your product is missing any of them at launch, you are not ready to launch.

Anand Trivedi, VP of Operations and Delivery at Radixweb say about these features, "In every fintech engagement we have delivered, the products that reached market fastest had one thing in common: every feature on this list was scoped in from day one. Not deferred. Not something that can be taken up in phase 2.” He further adds, “When compliance infrastructure and fraud detection are built into the architecture from the start, the launch is cleaner, the regulatory review is faster, and the post-launch firefighting simply does not happen."

Advanced User Authentication and Identity Verification

What it includes:

- Biometric authentication (fingerprint, face ID)

- Multi-factor authentication (MFA)

- Passkey-based login replacing traditional passwords

- Automated KYC verification embedded directly in the onboarding flow

- Real-time document verification and identity proofing

Why it is non-negotiable: Weak authentication in a fintech product is not a user experience problem. It is a regulatory liability, a reputational risk, and in most markets, a compliance failure. KYC must satisfy regulatory requirements across every jurisdiction you operate in, not just your home market.

Real-Time Transaction Processing

What it includes:

- High-throughput, low-latency backend architecture

- Automated failover with no single points of failure

- Event-driven processing that responds to transactions as they happen

- Continuous performance monitoring with automated alerting

Why it is non-negotiable: Building real-time processing capability correctly from the start costs a fraction of what retrofitting it into a batch-processing architecture costs later. This is one of the most expensive technical decisions to reverse in fintech software development.

AI-Powered Fraud Detection and Risk Scoring

What it includes:

- Machine learning models trained on transaction behavior patterns

- Real-time anomaly detection before transactions complete

- Continuous model improvement through investigation feedback loops

- Risk scoring integrated across onboarding, transactions, and account management

Why it is non-negotiable: Static, rule-based fraud systems cannot keep pace with the sophistication of modern financial crime. AI-powered fraud detection is the production standard in 2026. The businesses moving fastest on this are those who understand this very well. Any fintech product still relying on rule-based systems alone is operating with a known and growing security gap.

Compliance and Regulatory Reporting Modules

What it includes:

- AML transaction monitoring

- Suspicious activity report (SAR) generation

- Automated regulatory submissions

- Tamper-evident audit trails covering every transaction and user action

Why it is non-negotiable: Compliance reporting infrastructure cannot be built on demand when regulators ask for it. By that point it is already too late. It must be architected into the product from day one, covering every jurisdiction where you operate.

Data Visualization and Financial Analytics

What it includes:

- Real-time dashboards for end users (spending patterns, account health, portfolio performance)

- Operations dashboards for internal teams (risk exposure, compliance metrics, transaction volumes)

- Exportable reporting for enterprise and B2B clients

Why it is non-negotiable: In B2B fintech products, the quality of the analytics layer is frequently the primary buying criterion. In consumer fintech, users who cannot understand their own financial data at a glance do not stay engaged with the product. Analytics is not a reporting tool. It is a retention and conversion driver.

Multi-Currency and Multi-Market Support

What it includes:

- Multiple currency handling across transactions, balances, and reporting

- Support for multiple payment rails (SWIFT, SEPA, local real-time payment networks)

- Configurable compliance rules by jurisdiction

- Localized user experience by market

Why it is non-negotiable: Retrofitting multi-currency support into a single-currency architecture is one of the most expensive mistakes in fintech software development. If there is any possibility your product will operate across markets, build for it from the start. The cost of doing it later is three to five times higher than doing it correctly upfront.

API Integration Layer

What it includes:

- Connectors to payment networks (Visa, Mastercard, local rails)

- Identity verification provider integrations (Jumio, Onfido, Sumsub)

- Credit bureau and open banking data connections

- Accounting platform and ERP integrations

- Data aggregator connectivity (Plaid, Tink, Yodlee)

Why it is non-negotiable: Modern fintech products do not operate in isolation. They are nodes in a broader financial services ecosystem. A well-designed API integration layer that accommodates new third-party services without requiring fundamental architecture changes is not a technical nice-to-have. It is a core commercial requirement that determines how quickly your product can respond to market opportunities and partnership demands.

Fintech Regulations: What Your Business Must Comply With

Regulatory compliance is the single most underestimated cost and risk factor in fintech software development. It is, also one of the most common software development challenges facing financial organizations. Businesses that treat it as an afterthought consistently face delays and remediation costs. So, make sure you understand the regulatory landscape before you pay some to write even a line of code

Global Regulations That Apply Across Most Fintech Products

- PCI DSS (Payment Card Industry Data Security Standard) applies to any system that stores, processes, or transmits cardholder data. There are four compliance levels, and the requirements become progressively more demanding as your transaction volume increases. PCI DSS certification is mandatory for any product that handles card payments. The specific obligations for your transaction tier are defined in the PCI Security Standards Council's official compliance documentation, which outlines requirements across all four merchant levels.

- GDPR (General Data Protection Regulation) applies to any business collecting or processing the personal data of EU residents, regardless of where your business is based. GDPR shapes fundamental data architecture decisions: where data is stored, how long it is retained, who can access it, and what rights users have to request its deletion. GDPR enforcement intensified significantly in 2025, and fines for non-compliance now routinely reach the tens of millions of euros for fintech companies.

- KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements apply across virtually all fintech products that handle financial transactions. These are not merely compliance checkboxes. They are operational functions that must be built into your onboarding and ongoing monitoring infrastructure, with the capability to generate suspicious activity reports and cooperate with financial intelligence unit requests.

Fintech Regulations in the United States

- Bank Secrecy Act (BSA) and Anti-Money Laundering Act (AMLA) govern AML compliance for US financial institutions and their technology providers.

- Electronic Fund Transfer Act (EFTA) regulates electronic fund transfers and provides consumer protections for digital payment products.

- Fair Credit Reporting Act (FCRA) applies to any business that accesses or uses consumer credit data, which is highly relevant for fintech products in the lending and credit scoring space.

- Electronic Signatures in Global and National Commerce Act (ESIGN) governs the use of electronic signatures in financial transactions.

Fintech Regulations in the European Union

- PSD2 (Revised Payment Services Directive) is the foundational open banking regulation in Europe, mandating that banks expose account data and payment initiation capabilities through APIs to licensed third parties.

- DORA (Digital Operational Resilience Act) came into force in early 2025 and imposes strict requirements on IT risk management, incident reporting, and third-party technology risk for financial institutions and their software providers operating in the EU.

- MiCA (Markets in Crypto-Assets Regulation) creates a comprehensive licensing regime for crypto-asset businesses operating in the EU. The transitional period runs through mid-2026, after which unlicensed operation is not possible.

- EU AML Directives (AMLDs) set the baseline AML compliance standards for financial institutions across EU member states.

Fintech Regulations in the United Kingdom

- Financial Services and Markets Act 2000 (FSMA) provide the primary regulatory framework for financial services in the UK, overseen by the Financial Conduct Authority. Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017 (MLR 2017) govern AML compliance for UK-regulated businesses.

- Proceeds of Crime Act 2002 (POCA) imposes criminal liability for businesses that facilitate money laundering, making AML compliance a matter of legal survival, not just regulatory compliance.

Fintech Regulations in India

- Reserve Bank of India (RBI) guidelines govern digital payment systems, prepaid payment instruments, account aggregators, and peer-to-peer lending platforms.

- The Payment and Settlement Systems Act 2007 provides the legal framework for payment systems operators.

- DPDP (Digital Personal Data Protection) Act 2023, which came into force in 2024, creates a comprehensive framework for personal data processing in India that has significant implications for fintech companies collecting financial and identity data from Indian users.

How Much Does Fintech Software Development Cost?

I’m yet to sit in a project discussion where cost isn’t the first thing on the client’s mind. Business leaders need to know how much money they’ll need to invest, what ROI they can expect, and how soon. But I’ve seen more fintech developments guides try to dodge that question.

Now, I’ll be honest, it is not possible for me to give you a single number right now. Fintech software development costs vary enormously based on the type of product you are building, your compliance requirements, your target markets, and where your development team is based.

But what I can tell you are ballpark figures (realistic and grounded!) and a breakdown based on current market rates and what we’ve seen across our projects:

MVP and Proof-of-Concept Stage

- Cost range: USD 50,000 to USD 120,000

- Minimum cost for regulated products: USD 80,000

- Timeline: 2 to 4 months

A fintech MVP is designed to validate a core business concept with real users on a single platform, with basic features and minimum viable compliance. It is not a finished product. It is the fastest and most cost-efficient way to test whether your core assumption is commercially viable before committing to a full-scale build.

For regulated products, compliance requirements do not shrink because the product is at MVP stage. A payment product requiring PCI DSS compliance and a lending product requiring KYC integration must meet those obligations from day one, regardless of how lean the overall scope is. Regulators do not offer an exemption for early-stage products, and skipping compliance at MVP stage does not save money. It creates remediation costs that are significantly higher than doing it correctly the first time.

Mid-Scale Business-Ready Platform

- Cost range: USD 120,000 to USD 250,000

- Timeline: 5 to 9 months

- Best for: Funded startups launching their first commercial product, financial institutions launching a new digital service, or established businesses building their first embedded finance product.

A mid-scale platform is not a proof of concept. It is a commercially viable product built to operate under real regulatory scrutiny, handle genuine transaction volume, and retain paying users over the long term. Every architecture decision at this tier is made with scale and compliance in mind, not just speed to market.

Enterprise Platform

- Cost range: USD 300,000 and above

- Timeline: 9 to 14 months for initial release, with continuous development thereafter

- Annual maintenance cost: 15 to 20 percent of initial build cost

Enterprise platforms are the right investment for established financial institutions launching a new digital service, well-funded fintech companies scaling beyond their initial product market, and non-financial enterprises building a full embedded finance capability with multiple product lines. This is not the right starting point for a business that has not yet validated its core product with real users in a live market.

What Drives Costs Up

When I sit with clients to discuss budgets, I always give clear estimates. But I also walk them through the factors that can push costs beyond the original scope. Pratik Mistry, our EVP of Technology Consulting, has a way of explaining this that tends to land well in those conversations. He says, “Building a fintech product is like applying for a banking license. Everyone prices the application. Nobody budgets for the compliance audit, the capital requirements, and the six months of back-and-forth with the regulator that determine whether you actually get it.”

The factors that most consistently drive costs beyond initial estimates are:

1. Compliance and security architecture (30 to 40 percent of total project cost)

Compliance and security architecture alone can account for 30 to 40 percent of total fintech development costs, making it the single largest hidden budget driver in most projects. KYC integration, AML monitoring, penetration testing, and audit trail infrastructure are not optional line items you can defer to a later release.

2. Post-launch operational costs (USD 30,000 to USD 100,000 per year)

Most fintech budgets account for the build cost and nothing beyond it, which is where the financial surprises begin. API subscription fees, cloud infrastructure, compliance monitoring tools, security audits, and licensing maintenance frequently total USD 30,000 to USD 100,000 per year for a mid-scale fintech product, and that figure grows as your user base and transaction volume scales.

3. Development partner location (2x to 4x cost variance)

Choosing the right development partner location is one of the most powerful budget levers available to you, with hourly rates varying significantly by region and working with a team that brings 26 years of fintech engineering experience within a cost-efficient model often delivers better outcomes than chasing the lowest hourly rate.

Experienced fintech developers charge USD 30 to USD 50 per hour in South and Southeast Asia, USD 50 to USD 90 in Eastern Europe, USD 45 to USD 75 in Latin America, and USD 100 to USD 200 in North America and Western Europe for comparable technical capability.

Cost Comparison by Fintech Software Type and Development Region

The table below provides approximate baseline cost ranges for common fintech software types. These are starting points. Final costs depend heavily on feature scope, compliance requirements, and the development region you choose.

| Fintech Software Type | Asia | Eastern Europe | North America |

|---|---|---|---|

| Banking Software | USD 120,000 to USD 180,000 | USD 150,000 to USD 220,000 | USD 280,000 to USD 400,000 |

| Lending Software | USD 80,000 to USD 120,000 | USD 120,000 to USD 180,000 | USD 200,000 to USD 280,000 |

| Payment Processing Software | USD 60,000 to USD 100,000 | USD 90,000 to USD 150,000 | USD 150,000 to USD 250,000 |

| InsurTech Software | USD 60,000 to USD 90,000 | USD 80,000 to USD 130,000 | USD 130,000 to USD 200,000 |

| WealthTech and Investment Platform | USD 90,000 to USD 140,000 | USD 120,000 to USD 190,000 | USD 190,000 to USD 300,000 |

Two things to factor into your budget before finalizing numbers:

- Enterprise platforms exceed all ranges shown above significantly. The figures in this table reflect business-ready products, not full-scale enterprise deployments with multi-jurisdiction compliance and high-volume infrastructure.

- Annual maintenance costs should be budgeted separately at 15 to 20 percent of the initial build cost. This covers compliance updates, security patching, infrastructure scaling, and third-party API changes that occur after launch.

Build In-House, Outsource, or Partner: How to Decide

This is one of the most consequential decisions a business leader makes when approaching fintech software development. The right answer depends on your timeline, your budget, your existing technical capability, and your risk tolerance.

If you are looking for a starting point to guide your decision, here’s the only table you need to see:

| Model | Best For | Main Advantage | Main Risk |

|---|---|---|---|

| Build In-House | Large FIs with long-term, ongoing dev needs | Full control and IP ownership | High recruitment cost; specialist scarcity |

| Outsource to Specialist | First fintech product, new market entry, speed | Faster time to market; proven compliance knowledge | Partner selection risk |

| Hybrid Model | Established businesses with internal product lead | Direction control + engineering depth | Coordination overhead |

Build In-House

Building an in-house fintech development team makes sense when you are a large financial institution with ongoing, long-term product development needs, where the cumulative cost of an internal team over three to five years is lower than sustained outsourcing.

However, the challenge here is that specialist fintech engineers combining domain knowledge with compliance expertise and modern cloud-native architecture experience are in extremely short supply and command premium salaries. Most businesses significantly underestimate both the time required to recruit a capable team and the ongoing cost of retaining them in a competitive talent market.

Outsource to a Specialist Fintech Development Company

Outsourcing to a specialist fintech software development company is the most cost-effective and low-risk approach for businesses that are building their first fintech product, launching into a new market, or need to accelerate development beyond what their internal team can deliver. The key word is specialist. A general software development company that happens to list fintech in its service portfolio is not the same as a company that has built dozens of regulated financial products and navigated real compliance audits. This core fintech expertise and experience is what separates the strongest fintech development companies from the rest.

When evaluating a fintech software development company as a partner, the questions that matter most are:

- Have they built products in your specific fintech category?

- Can they provide references from clients who have successfully passed regulatory audits?

- Do they have dedicated expertise in the compliance standards that apply to your market?

- What does their security testing and penetration testing process look like?

- Do they treat compliance as an architecture decision or an afterthought?

Hybrid Model

Many established businesses find that the most effective model is a hybrid approach: an internal product manager and domain lead who owns the vision and the relationship with regulators, combined with an external specialist development team that owns the engineering. This model gives you control over product direction without requiring you to build and maintain a full engineering capability.

How to Choose a Fintech Software Development Company

The choice of development partner is the single variable most correlated with fintech project success or failure, and the track record that separates strong candidates from the rest is most visible in how they have handled banking app development for institutions operating under real regulatory scrutiny. Here is a practical framework for evaluating your options.

Evaluate Fintech Domain Depth, Not General Capability

A development partner's general software capability is necessary but not sufficient for fintech. You need a partner who understands the specific compliance requirements, security architecture patterns, and integration ecosystems of your fintech category. Ask to see case studies from projects in your specific category, not their broader portfolio.

Demand Evidence of Compliance Expertise

If a development partner does not bring up PCI DSS, KYC, AML, or the specific regulatory framework for your market in the first conversation, that is a serious warning sign. A partner who treats compliance as a downstream concern will cost you significantly more in remediation costs.

Assess Security Architecture Capability

Security in fintech is a deeply technical discipline: threat modelling during design, penetration testing before every major release, zero-trust network architecture, and comprehensive audit logging. Ask potential partners to walk you through their security development lifecycle in detail.

Look for Long-Term Partnership Orientation

Fintech software development is not a project — it is an ongoing commitment. Regulators update requirements. Fraud patterns evolve. New payment rails emerge. Partners who invest in knowledge transfer, documentation quality, and code maintainability deliver fundamentally different long-term outcomes than partners optimising for delivery speed on initial scope.

Check Delivery Track Record

How many fintech products has this partner taken from design to production deployment? What has been their experience with regulatory audits? Have their clients had compliance issues traced back to development work? The answers reveal far more than any sales presentation.

Common Fintech Business Challenges and How to Navigate Them

Every business building fintech software faces a recognizable set of challenges. While some of these challenges are avoidable with proper planning, others need to be handled as and when they arise. But know what these challenges are and what you can realistically do to tackle those is what separates business that are able to face these and those that succumb under pressure.

Based on what I have seen time and again across multiple fintech software projects, the key challenges include:

Regulatory Complexity Across Multiple Markets

Operating across more than one regulatory jurisdiction multiplies compliance complexity non-linearly. GDPR applies in the EU, CCPA in California, RBI guidelines in India, FCA rules in the UK. Each has different data residency, consent, and reporting requirements. Businesses that attempt to navigate multi-jurisdictional compliance without specialized legal and compliance expertise routinely delay their launches by six to twelve months. Building compliance into your architecture as a modular, configurable layer rather than hard-coded to a single market is the right long-term approach.

Legacy System Integration

For financial institutions building new digital products on top of existing infrastructure, legacy system integration is frequently the most technically complex and expensive part of the project. Core banking systems built on decades-old architecture were not designed to expose APIs to modern fintech products, and modernizing these connections is a core capability of experienced custom software development teams who have handled similar migrations across financial institutions.

Cybersecurity at Scale

As your fintech platform grows, it becomes a more attractive target for sophisticated financial crime. Security must be treated as a continuous investment, not a one-time project cost. Production fintech platforms require continuous security monitoring, regular penetration testing, vulnerability management programs, and incident response planning. Businesses that invest in security infrastructure during the build phase spend significantly less than those who respond to breaches reactively.

Building Trust with Users at Scale

Trust is the most valuable asset in financial services. Building it requires more than good security. It requires transparent communication about how user data is used, consistent uptime, clear and responsive customer support, and a track record of handling edge cases fairly. Fintech products that rush to market without the operational infrastructure to support trust at scale consistently suffer higher churn and lower lifetime value than their more patient competitors.

Talent Scarcity in Fintech Engineering

The combination of compliance knowledge, cloud-native engineering experience, and security expertise required for serious fintech software development is genuinely rare in the market. This is the strongest practical argument for working with a specialist fintech development partner rather than attempting to hire a full team independently. The time and cost of recruiting, onboarding, and retaining the specialists required for a quality fintech build typically exceeds the cost of outsourcing to an experienced partner by a significant margin.

These are not just theoretical risks. They are the conversations I have with clients every week. At Radixweb, we have navigated every one of them and the businesses that come to us early consistently spend less, launch faster, and hit fewer walls than those who bring us in to fix what went wrong. If any of these challenges are already on your radar, that is exactly the right time to talk.

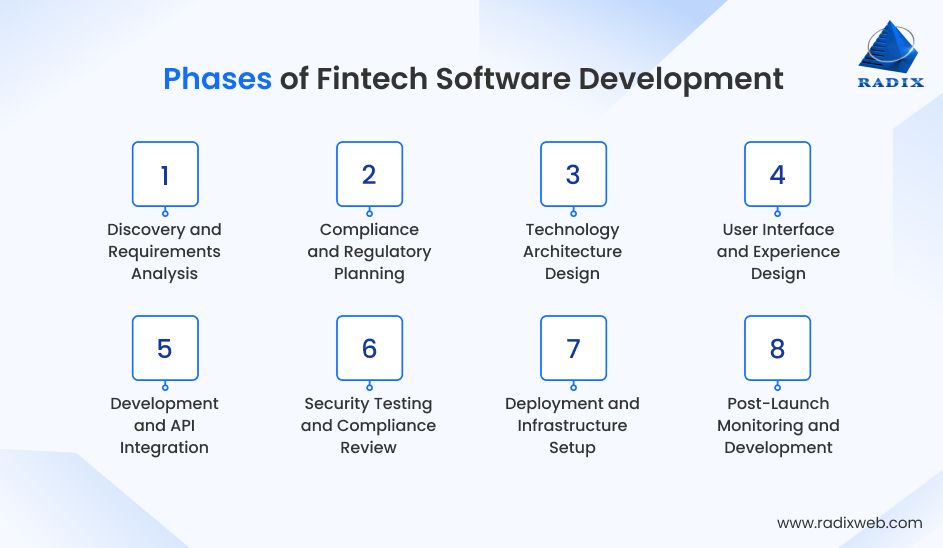

Fintech Software Development Process: What to Expect

A fintech software project follows a structured lifecycle, where early-stage decisions have a disproportionate impact on cost, compliance, and scalability. Understanding how a fintech software development project actually unfolds helps you set realistic expectations, allocate budget correctly, and engage meaningfully with your development partner at each stage.

Phase 1: Discovery and Business Requirements Analysis

Every serious fintech project begins with a structured discovery phase. This involves mapping your business objectives to specific product features, identifying your regulatory obligations in each target market, scoping the integration requirements with third-party systems, and defining your compliance and security architecture at a high level. Discovery typically takes two to six weeks and is the most important investment you make in the entire project. Decisions made during discovery determine the cost, timeline, and quality of everything that follows.

Phase 2: Compliance and Regulatory Planning

Before any design or development begins, your regulatory obligations must be fully understood and mapped to specific technical requirements. Which data must be collected during onboarding? Where must it be stored? What audit trails are required? What reporting obligations does your product create? Answering these questions before the design phase begins is the difference between a compliant product and a product that requires expensive remediation before it can launch.

Phase 3: Architecture Design

Your technology architecture defines the capabilities, the scalability limits, the security posture, and the long-term maintainability of your fintech product. Cloud-native architecture on platforms like AWS, Azure, or Google Cloud is the default choice for new fintech products in 2026, and teams that combine cloud infrastructure expertise with deep domain knowledge in fintech app development are best positioned to deliver both the technical and compliance requirements simultaneously, given the reliability, scalability, and security tooling these platforms provide. Microservices architecture is the appropriate choice for products that will need to scale components independently or integrate multiple financial service types into a unified platform.

Phase 4: UI and UX Design

User experience in fintech is a trust signal. Users who find a financial interface confusing or opaque do not give it the benefit of the doubt. They leave. Fintech UX design must balance simplicity of interaction with the complexity of the underlying financial operations, communicate security clearly without creating friction, and meet accessibility standards across all target markets. Mobile-first design is the default for consumer fintech products in 2026. Desktop interfaces remain important for B2B and enterprise fintech tools.

Phase 5: Development and Integration

Development in a professional fintech project follows an agile methodology, with regular sprint reviews that allow the business to review progress, reprioritize features, and course-correct before the project reaches its final stages. API integrations with payment networks, identity verification providers, banking infrastructure, and third-party data sources are built and tested at this stage.

Phase 6: Security Testing and Compliance Review

Before any fintech product goes near a production environment, it must go through thorough security testing including penetration testing, vulnerability assessment, and a formal review of the compliance architecture by qualified specialists. This phase is not a formality. Security defects identified during testing cost a fraction of what the same defects cost if they are discovered in production.

Phase 7: Deployment and Infrastructure Setup

Production deployment of a fintech product requires careful planning around infrastructure resilience, backup and recovery procedures, monitoring and alerting systems, and the operational runbooks your team will use when things go wrong. Regulatory requirements in many jurisdictions now mandate specific recovery time and recovery point objectives, meaning that your infrastructure design must account for audit requirements, not just technical performance.

Phase 8: Post-Launch Monitoring and Continuous Development

A fintech product does not stop evolving at launch. Regulatory requirements change. Fraud patterns evolve. User expectations shift. New payment technologies emerge. The most successful fintech products treat their software as a living operational asset that requires continuous investment, not a project that ends at go-live.

The Future of Fintech Software Development

Three forces are already clearly shaping the direction of fintech software development over the next two to three years:

- AI as the primary interface layer: The prototypes of AI-powered financial advisors, AI-driven loan officers, and AI-based compliance monitoring operating in 2026 will become mainstream products within two to three years. Businesses investing in data infrastructure and AI integration capability today will have a structural advantage when these capabilities become standard competitive requirements.

- Compliance automation by necessity: The volume and complexity of global regulatory requirements will exceed the capacity of human compliance teams to manage manually. Businesses investing in RegTech integration and compliance-by-design architecture now will operate across more markets with less operational risk than competitors relying on manual processes.

- Embedded finance as the default business model: By 2028, the majority of high-volume digital businesses — in retail, healthcare, logistics, and professional services — will offer at least one embedded financial product. Businesses that build the technical foundation today will capture a disproportionate share of that opportunity.

Why Partner with Radixweb for Fintech Software Development

26+ years of experience in building software for regulated industriesAt Radixweb, our fintech software development practice combines deep compliance expertise with modern cloud-native engineering and a track record of delivering financial products that operate in production under real regulatory scrutiny. We have completed 4,500+ software projects across banking, payments, lending, and insurance. We treat compliance as an architecture decision, not a final checklist. And these are not just tall claims, you can see it in action across our fintech project deliveries.If you are building a fintech product and want a partner who will tell you the hard things early, someone who will not just tell you but walk you through the realities of compliance costs, architecture trade-offs, and what your timeline actually requires, that is the conversation I would like to have with you. Schedule an initial idea assessment session and let’s map where you are and what it takes to get where you are going.

Frequently Asked Questions

What is fintech software development?

How much does fintech software development cost?

How long does fintech software development take?

What regulations apply to fintech software development?

How do I choose a fintech software development company?

What is the difference between fintech software and banking software?

What is embedded finance and how does it relate to fintech software development?

Explore More Topics

Ready to brush up on something new? We've got more to read right this way.

Get top Insights and news from our technology experts.